(San Francisco) – Defining its plans for

re-establishing a common stock dividend in 2005, PG&E

Corporation (NYSE:PCG) has approved a dividend policy

and established a target annual dividend of $1.20 per

share, or $0.30 per share on a quarterly basis. The

company will hold a conference call with the financial

community at 11:30 a.m. Eastern time today to discuss

the announcement. The conference call will be open

to the public on a listen-only basis via webcast at

www.pgecorp.com.

Payment of the initial quarterly dividend will

be subject to an actual dividend declaration at a

later date. The declaration could be as early as

February 2005 if Pacific Gas and Electric Company

refinances part of its balance sheet as planned in

early 2005 through the issuance of Energy Recovery

Bonds (ERBs). The initial quarterly dividend payment

could then be as early as April 2005, with a total

of three dividend payments to shareholders for the year.

The refinancing through the issuance of the ERBs is

also expected to save Pacific Gas and Electric Company

customers up to $1 billion over the next eight years.

“Investors in PG&E Corporation can now see

increased specificity regarding the Corporation’s

plan to re-establish a common stock dividend as early

as possible in 2005,” said Robert D. Glynn, Jr.,

PG&E Corporation Chairman, CEO and President. “We

intend to return as much as $1.75 billion to shareholders

by the end of next year through dividends and stock

repurchases.”

The $1.20 per share target reflects the Corporation’s

policy to pay dividends at levels that strike a balance

among comparability with dividend yields and payout

ratios of similar utility companies, the ability to

sustain payments in the future, and the desire to retain

adequate financial flexibility to make investments

in its core business. The Corporation’s dividend

policy results in a target payout ratio of 50 percent

to 70 percent, relative to earnings per share from

operations.

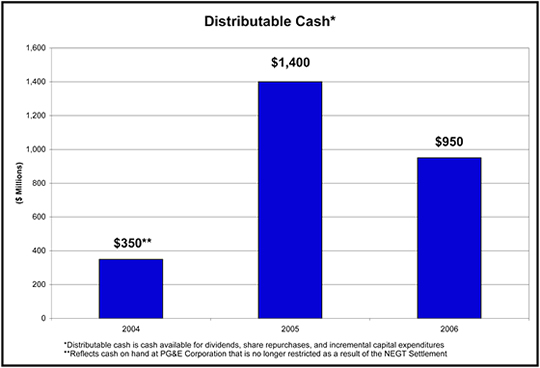

The Corporation will fund dividend payments and share

repurchases with distributable cash, which is cash

from operations that remains available after the company

funds capital expenditures and takes any action necessary

to ensure it maintains a balanced capital structure.

Assuming Pacific Gas and Electric Company issues ERBs

early next year to refinance part of its balance sheet,

PG&E Corporation estimates that $2.7 billion would

be available between now and the end of 2006 for distribution

to shareholders through dividends and stock repurchases,

as well as for incremental investments in its core

utility business.

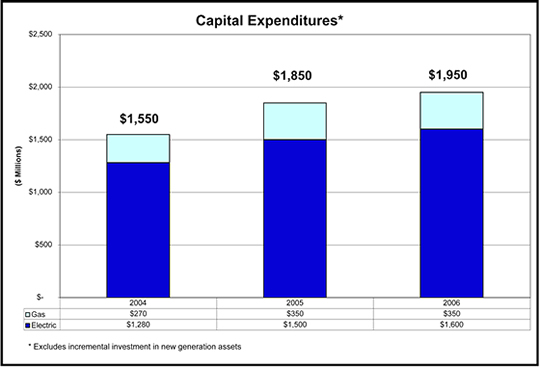

Underlying the Corporation’s projections is

its estimate that capital expenditures at Pacific Gas

and Electric Company will average $1.9 billion per

year for 2005 and 2006. (The company is actively evaluating

the potential for additional investments in new electric

generation, additional electric transmission infrastructure

and automated metering, which would increase capital

expenditures over current estimates.) Assuming average

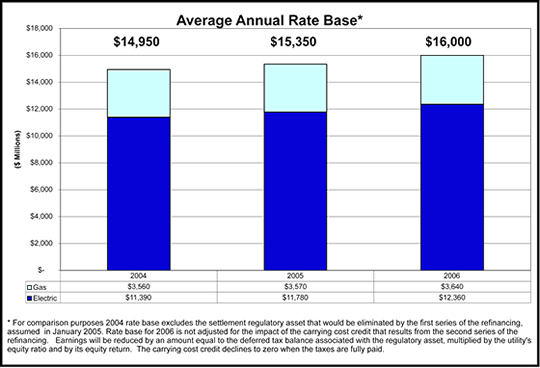

annual capital spending of $1.9 billion, Pacific Gas

and Electric Company’s average rate base will

increase at a rate of 3.4 percent per year from approximately

$15 billion in 2004 to $16 billion in 2006. The Corporation

also assumes that the equity portion of the utility’s

authorized capital structure will remain at 52 percent,

that the authorized return will remain at least at

11.22 percent, and that the utility earns the full

authorized rate of return. These and other financial

data are outlined in the attached charts and tables.

PG&E Corporation last declared a common stock

dividend in October 2000 for the fourth quarter of

that year. The last common dividend payment was made

in March 2001.

Please visit our website at www.pgecorp.com for more

information and instructions for accessing the conference

call webcast. The call will be archived at www.pgecorp.com.

Alternatively, a toll-free replay of the conference

call may be accessed shortly after the live call through

October 29, 2004, by dialing 877-690-2094. International

callers may dial 402-220-0649.

Supplemental Assumptions and Information

| <>Table 1: Assumptions 2005 - 2006 |

| Average Annual CapEx |

$1,900 million |

| ROE |

11.22% |

| Equity Ratio |

52% |

| Target Annual Initial Dividend |

$1.20 per share |

| Target Dividend Payout Range |

50% to 70% |

| ERB Issuance Target Dates |

January 2005 & January 2006 |

| <>Table 2: Select Cash Items |

| (Millions) |

| |

2004 |

2005 |

2006 |

| Capital Expenditures |

$1,550 |

$1,850 |

$1,950 |

| Distributable Cash* |

$350** |

$1,400 |

$950 |

| |

|

|

|

| * Distributable cash is cash available

for dividends, share repurchases, and incremental

capital expenditures compared to levels assumed

above. |

| **Reflects cash on hand at PG&E Corporation

that is no longer restricted as a result of the NEGT

settlement. |

| <>Table 3: Milestones |

| ERB Issuance |

|

| CPUC approval |

4th Quarter 2004 |

| Receipt of IRS PLR |

4th Quarter 2004 |

| SEC Approval |

4th Quarter 2004 |

| Issuance |

January 2005 |

| |

|

| Dividend Payout |

|

| Declaration |

1st Quarter 2005 |

| Dividend Payment |

April 2005 |

This press release contains forward-looking statements regarding the

anticipated payment of future common stock dividends and stock repurchases

based on various assumptions, including anticipated cash flows in 2005

and 2006. These statements are based on current expectations and assumptions

which management believes are reasonable and on information currently

available to management but are necessarily subject to various risks

and uncertainties. In addition to the risk that the assumptions (described

above) underlying the target dividend payout ratio and initial target

annual dividend amount prove to be inaccurate, other factors that could

cause actual results to differ materially from those contemplated by

the forward-looking statements include:

- The timing and resolution of the petitions for

review that were filed in the California Court of

Appeal seeking review of (i) the CPUC's December

18, 2003 decision approving the Settlement Agreement,

and (ii) the CPUC's March 16, 2004 denial of applications

for rehearing of the December 18, 2003 decision;

- The timing and resolution of the pending

appeals of the bankruptcy court's order confirming the

Utility’s

plan of reorganization under Chapter 11;

- Whether the conditions to issuing the ERBs are

met, and if so, the timing and amount of the issuance

of the ERBs;

- Whether the CPUC approves the Utility's long-term

electricity resource plan and adopts the Utility's

related ratemaking proposals, whether the assumptions

and forecasts underlying the long-term resource plan

prove to be accurate, and the terms and conditions

of the long-term resource commitments the Utility

enters into in connection with its long-term resource

plan;

- Unanticipated changes in operating expenses

or capital expenditures affecting the Utility’s

ability to earn its authorized rate of return;

- The level and volatility of wholesale electricity

and natural gas prices and supplies, the Utility's

ability to manage and respond to the levels and volatility

successfully, and the extent to which the Utility

is able to timely recover increased costs related

to such volatility;

- The extent to which the Utility is able

to recover its costs incurred in meeting its obligation to supply

electricity to customers, whether costs are incurred

to meet or manage the Utility’s residual

net open position (i.e., that portion

of the Utility's electricity customers' demand

not satisfied by electricity that the Utility generates

or has under contract, or by electricity provided

under the California Department of Water Resources’ electricity

contracts allocated to the Utility's customers)

or to ensure adequate resources as required by

the CPUC;

- The operation of the Utility's Diablo Canyon nuclear

power plant which exposes the Utility to potentially

significant environmental and capital expenditure

outlays;

- The impact of current and future ratemaking actions

of the CPUC, including the risk of material differences

between forecasted costs used to determine rates

and actual costs incurred;

- The extent to which the CPUC or the FERC delays

or denies recovery of the Utility's costs from customers

due to a regulatory determination that such costs

were not reasonable or prudent or for other reasons

resulting in write-offs of regulatory balancing accounts;

- How the CPUC administers the capital structure,

stand-alone dividend and first priority conditions

of the CPUC's decisions permitting the establishment

of holding companies for California investor-owned

electric utilities;

- The impact of future legislative or regulatory

actions or policies;

- Increased competition;

- The outcome of pending litigation; and

- Other factors discussed in PG&E Corporation's

and the Utility’s SEC reports.